37K+

5-star reviews from

FileInvite portal users

5-star reviews from

FileInvite portal users

Files securely collected

Average hours saved

per week, per user

Over 1 million FileInvite

portals served

Standardize complex loan packages with templates that automate requests, reminders, file naming and status updates. AI-powered intelligent email intake automatically matches forwarded documents to the correct customer, loan and request. Get correctly named, complete files faster with less rework, accelerating closings and reducing operational costs. FileInvite runs reliably in the background, making your borrower experience exceptional.

37k borrowers gave us five stars for a reason.

Coordinate document collection across borrowers, guarantors, co-borrowers, brokers, and attorneys. Send party-specific document requests with personalized checklists, track submissions in real-time, and route documents through your internal approval workflows. FileInvite maintains a complete audit trail across all parties, perfect for SBA 7(a) loans, commercial real estate deals, and syndicated transactions.

Assign tasks, share visibility, and collaborate seamlessly across loan officers, processors, underwriters, and credit analysts. Route documents for internal review, add comments and notes on submissions, and mention team members for quick coordination. Set role-based permissions to control who can approve, edit, or view invites, ensuring compliance while keeping deals moving efficiently through your pipeline.

Don't settle for less. A secure and reliable solution, FileInvite is SOC 2 Type II compliant, with 256-bit encryption, advanced user provisioning, and a 99.9% uptime guarantee. Our at rest and in transit encryption ensures that documents, messages and data are secured to the latest security standards. FileInvite is regularly subjected to stringent third party testing.

Choose between open or password protected borrower portals, and tailor internal roles and permissions to suit your security and privacy requirements. Stay compliant with a full history of client interactions, messages and files, and grant access to external auditors when required.

.png?width=723&height=586&name=security-compliance%20(1).png)

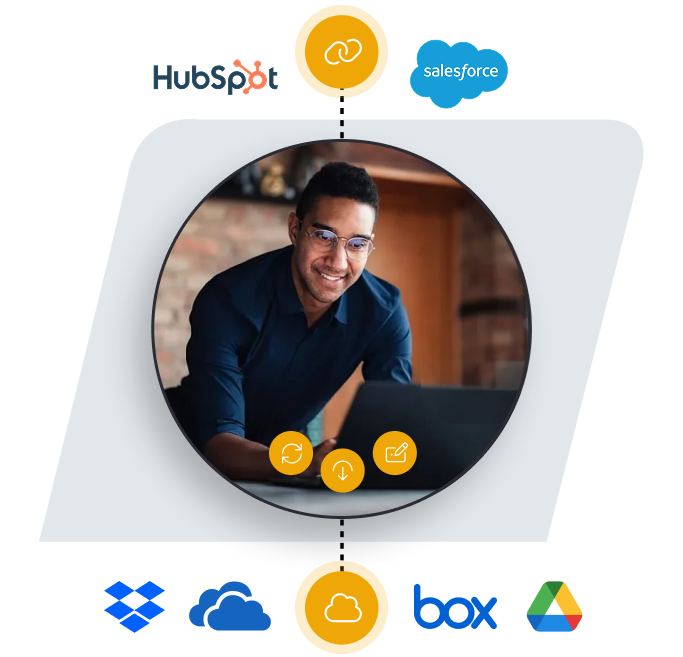

FileInvite's Connected Workflow Integrations allow you to initiate document requests, send messages, and manage workflows directly from Salesforce, Hubspot, and other CRM platforms. Connected Workflow Integrations are a no-code solution implemented by our own teams to speed up delivery and reduce costs and change management.

FileInvite integrates out-of-the-box with cloud storage solutions, including SharePoint, OneDrive, Box and Google Drive, to eliminate manual handling of borrower documents. FileInvite automatically converts all uploaded files to PDF format, securely syncs them to the cloud, and can dynamically rename and organize them to suit your folder and file name conventions.

Unlock a deeper level of integration with FileInvite's enterprise-grade API. Reduce cross-platforming by integrating FileInvite with your core, LOS, or your own internal systems to streamline workflows across multiple applications.

Coordinate document collection across borrowers, guarantors, co-borrowers, brokers, and attorneys. Send party-specific document requests with personalized checklists, track submissions in real-time, and route documents through your internal approval workflows. FileInvite maintains a complete audit trail across all parties, perfect for SBA 7(a) loans, commercial real estate deals, and syndicated transactions.

Assign tasks, share visibility, and collaborate seamlessly across loan officers, processors, underwriters, and credit analysts. Route documents for internal review, add comments and notes on submissions, and mention team members for quick coordination. Set role-based permissions to control who can approve, edit, or view invites, ensuring compliance while keeping deals moving efficiently through your pipeline.

Don't settle for less. A secure and reliable solution, FileInvite is SOC 2 Type II compliant, with 256-bit encryption, advanced user provisioning, and a 99.9% uptime guarantee. Our at rest and in transit encryption ensures that documents, messages and data are secured to the latest security standards. FileInvite is regularly subjected to stringent third party testing.

Choose between open or password protected borrower portals, and tailor internal roles and permissions to suit your security and privacy requirements. Stay compliant with a full history of client interactions, messages and files, and grant access to external auditors when required.

FileInvite's Connected Workflow Integrations allow you to initiate document requests, send messages, and manage workflows directly from Salesforce, Hubspot, and other CRM platforms. Connected Workflow Integrations are a no-code solution implemented by our own teams to speed up delivery and reduce costs and change management.

FileInvite integrates out-of-the-box with cloud storage solutions, including SharePoint, OneDrive, Box and Google Drive, to eliminate manual handling of borrower documents. FileInvite automatically converts all uploaded files to PDF format, securely syncs them to the cloud, and can dynamically rename and organize them to suit your folder and file name conventions.

Unlock a deeper level of integration with FileInvite's enterprise-grade API. Reduce cross-platforming by integrating FileInvite with your core, LOS, or your own internal systems to streamline workflows across multiple applications.

Coordinate document collection across borrowers, guarantors, co-borrowers, brokers, and attorneys. Send party-specific document requests with personalized checklists, track submissions in real-time, and route documents through your internal approval workflows. FileInvite maintains a complete audit trail across all parties, perfect for SBA 7(a) loans, commercial real estate deals, and syndicated transactions.

Assign tasks, share visibility, and collaborate seamlessly across loan officers, processors, underwriters, and credit analysts. Route documents for internal review, add comments and notes on submissions, and mention team members for quick coordination. Set role-based permissions to control who can approve, edit, or view invites, ensuring compliance while keeping deals moving efficiently through your pipeline.

Don't settle for less. A secure and reliable solution, FileInvite is SOC 2 Type II compliant, with 256-bit encryption, advanced user provisioning, and a 99.9% uptime guarantee. Our at rest and in transit encryption ensures that documents, messages and data are secured to the latest security standards. FileInvite is regularly subjected to stringent third party testing.

Choose between open or password protected borrower portals, and tailor internal roles and permissions to suit your security and privacy requirements. Stay compliant with a full history of client interactions, messages and files, and grant access to external auditors when required.

FileInvite's Connected Workflow Integrations allow you to initiate document requests, send messages, and manage workflows directly from Salesforce, Hubspot, and other CRM platforms. Connected Workflow Integrations are a no-code solution implemented by our own teams to speed up delivery and reduce costs and change management.

FileInvite integrates out-of-the-box with cloud storage solutions, including SharePoint, OneDrive, Box and Google Drive, to eliminate manual handling of borrower documents. FileInvite automatically converts all uploaded files to PDF format, securely syncs them to the cloud, and can dynamically rename and organize them to suit your folder and file name conventions.

Unlock a deeper level of integration with FileInvite's enterprise-grade API. Reduce cross-platforming by integrating FileInvite with your core, LOS, or your own internal systems to streamline workflows across multiple applications.